The securitization of the Federal Government’s N23.7 trillion Ways and Means may trigger stronger macroeconomic headwinds, with extensive repercussions on the country’s productivity and financial stability.

The National Assembly last week approved President Muhammadu Buhari’s request to securitize outstanding government Ways and Means of N22.7 trillion due to the Central Bank of Nigeria (CBN), It also received approval for an additional N1 trillion Ways and Means advances for the implementation of the 2022 Supplementary Appropriation Act as passed by the National Assembly.

The CBN Act, of 2007 provides a window for “Ways and Means”, essentially a stop-gap funding window for overdrafts from the apex bank to the Federal Government, subject to a limit of five percent of the previous year’s revenue size.

Analysts at the weekend said the securitization of the ballooning Ways and Means could be a bitter-than-sweet measure, with possible negative implications on general economic performance and access to funding by governments and private operators.

The investment banking group, Afrinvest (West Africa) said the securitization could turn out to be a landmark or landmine for the economy, with many negative implications for the economy and the citizenry.

With the securitization, the CBN would become a constitutionally recognized long-term creditor to the Federal Government. Under the approval, the total outstanding Ways and Means of about N23.72 trillion would be structured into a long-term issuance from the federal government to the CBN with key terms, including tenure of 40 years; moratorium on principal repayment of three years; and pricing or interest rate fixed at nine percent yearly.

Afrinvest noted that the securitization evidenced the inability of the outgoing administration to offset what should have been a stop-gap funding from the CBN.

“Noteworthy, 96.2 percent or N21.8 trillion of the gross Ways & Means liability was obtained within the eight years of the outgoing administration-2015 – 2022, a gross violation of the allowable five percent of the previous year’s revenue limit imposed by section 38 of CBN’s Act, 2007,” Afrinvest stated.

According to analysts, with the securitization approval coming less than 30 days before the swearing-in of a new administration and Nigeria’s dwindling national revenue amid rising loan-servicing costs, there could be many negative implications for the economy.

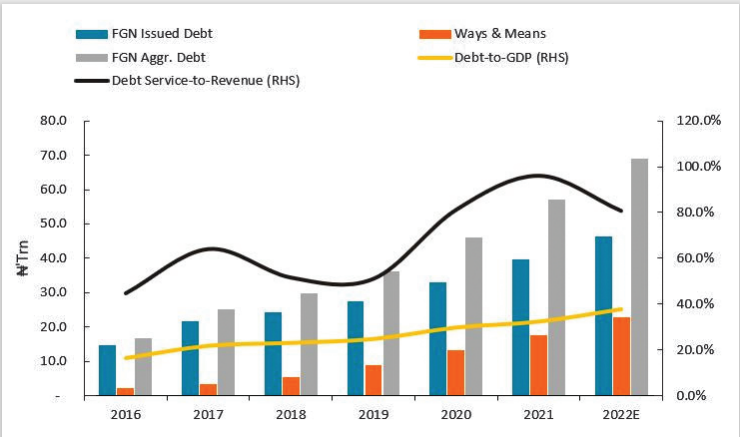

“First, Nigeria’s total debt profile has surged by 32.9 percent to N69 trillion, translating to an increase in debt per capita from N210,227 to N313,409 assuming a population size of 220 million. With very little infrastructural development to show for the 96.2 percent and 310.8 percent increases in Ways & Means liability and other borrowings respectively in the last eight years, the securitization approval has just passed on the liability, especially principal payment at maturity, to the young and future generation.

“Second, though the reduced interest payment cost on the Ways & Means liability, now nine percent as against the previous 300 basis points above Monetary Policy Rate, and the three years moratorium window provided in the restructuring terms should reduce the cost of debt servicing in the near-term, budget and fiscal deficit sizes may not in any way reduce due to Federal Government’s u-turn on Premium Motor Spirit (PMS) subsidy removal by mid-year. PMS subsidy is estimated to gulp N6.8 trillion in 2023,” Afrinvest stated.

Analysts said the securitization and continuation of petrol subsidies could create extended apathy from foreign investors and bilateral lenders towards Nigeria in the near term.

“Hence, should the Federal Government’s projected revenue underperform going forward, as the trend has been historically, deficit plugging would mostly be done through domestic debt issuance, and by extension, crowd out local businesses which are major drivers of Gross Domestic Products (GDP) growth,” Afrinvest concluded.

Cordros Capital said the securitization of the Ways and Means as part of the balance sheet of the CBN raises a “moral hazard issue”.

Cordros Capital, however, noted that the conversion would ensure that “the public debt profile reflects its true picture, bringing debt sustainability to the forefront of policymaking and, possibly, ensuring the next administration consciously embark on fiscal consolidation”.

Analysts at Cordros Capital said they were not surprised by the decision to suspend the subsidy removal given how the administration has delayed the decision over the past three years.

“Indeed, we stated in our 2023 fiscal year domestic macroeconomic outlook that our base case scenario is for the incoming administration to embark on partial subsidy removal as it is unlikely the administration will follow through with removing the PMS subsidy by June 2023.

“Besides, our view for partial subsidy removal by the incoming administration is premised on the lingering acute domestic price pressures amid the need to avoid public protests at the start of a new administration,” Cordros Capital stated.

President, of Capital Market Academics of Nigeria, Professor Uche Uwaleke, said the securitization has many positive parts but called for an overhaul of the Ways and Means framework to avoid a reoccurrence of the huge unbudgeted borrowing.

“Be that as it may, it’s important that going forward, adequate safeguards are put in place to ensure that CBN’s Ways and Means are curtailed due to its negative impact on the general price level. The relevant provisions of the CBN Act should clearly stipulate the conditions under which debt limits can be breached, the process which should involve approval by the National Assembly as well as stiff sanctions for breach of the limits provided in the Act without following due process,” Uwaleke said.

According to him, the securitization of CBN’s Ways and Means, on the positive side, affords the government a breather in terms of debt service burden in view of the fact that repayment of over N22 trillion will now be spread over 40 years with a three year grace period on the principal sum.

“Similarly, the cost of annual debt service will reduce given the concessional rate of 9.0 percent as against the current 20.5 percent interest rate charged on CBN’s Ways and Means. The cumulative effect of these would be a reduction in the government budget deficit and the freeing up of resources that could be applied to more productive areas.

“It’s also important to note that since the securities will only be taken up by the CBN and not the public, the fear that it will crowd out the private sector is no longer there. There’s equally the issue of debt transparency that it engenders. Before now, CBN’s Ways and Means did not form part of the public debt stock reported by the Debt Management Office (DMO). Securitisation would entail including it as part of the country’s public debt which makes for transparency,” Uwaleke, a professor of capital market studies and Don at Nassarawa State University, stated.

{kind=link}